Pension Funds & Private Market

Why?

In my 3 years of career as a founder of a startup, one of the few reasons that kept me going despite the ups and downs was witnessing huge potentials being realised.

I also came to realise that while the tech industry was solving many of the most difficult problems of our times, and while the public is enjoying the benefits through using their services and products (such as better phones, shopping experience, SaaS…etc), the capital reward was still largely concentrated to the handful of founders and their early investors. In this sense, the technology entrepreneurs, many of whom are liberal democrats, aren’t free from the argument that the technology industry is exacerbating one of the biggest problems of capitalism: wealth inequality. But could it change? How could it change without taking away the benefits of capitalism and the motivation that drives the entrepreneurs?

I have a conviction that our world is transitioning to a technology-driven decentralised and democratised world (read about it here) and that such transition is already happening and will continue to be the trend in almost all industries (read about how it's impacting the media industry here and banking here). I also believe private market investment (including early-stage venture investments) are no exception to this trend. The question is, how and in what form would this transition occur in the private investment market?

While there are some early forms that allow the public to invest in startups, one of the most efficient and effective ways for the transition could happen without exacerbating the inequality problem is by large public institutions taking increased interest in private equity (PE, including venture capital) sectors and one such institution is pension funds. In fact, we are now seeing many pension funds increase their exposure to private equity markets; pressured by unfavourable demographic changes (reduction in the number of contributors and increase in beneficiaries), subdued earnings prospect in traditional assets and exceptional value being created from private markets.

In this writing, I will look further at why pension funds should (and some have already) increase exposure to PE sector and how this could be achieved. I will close it with some of the remaining questions that warrant further study.

I will be using CPP as a source for some data because 1) I am a Canadian citizen and 2) CPP is one of the largest national pension fund (AUM of $450B as of Q3 2020) in the world.

What?

Change in demographics

As you can see from Figure 1, the net cash flow for the CPP plan is expected to turn negative in ~30 years time (that is combining the base and additional CPP. You can read more about the introduction of the additional CPP in 2019 and its rationale in CPP’s 2020 annual report here).

By and large, the main driver for this negative trend is correlated with how the demographic is changing unfavourably in Canada. According to the CPP’s 2019 actuarial report (link here), the total number of contributors to CPP is expected to increase from 14.5M in 2019 to 18.4M in 2050, a 26.9% increase. The total number of beneficiaries, on the other hand, is expected to increase by 224.1% or from 5.8M in 2019 to 18.8M in 2050. The same actuarial report also projects that the total dollar amount for contribution will increase by 288.1% while the total dollar expenditure will increase by 339.9% over the same period.

This means that the fund’s reliance on income generated from its investment income will gradually increase. Today, CPP’s revenue portion from the investment income is 26% but this is expected to be 41% and 70% for base CPP and additional CPP, respectively, by 2075.

Change in return characteristics among asset classes

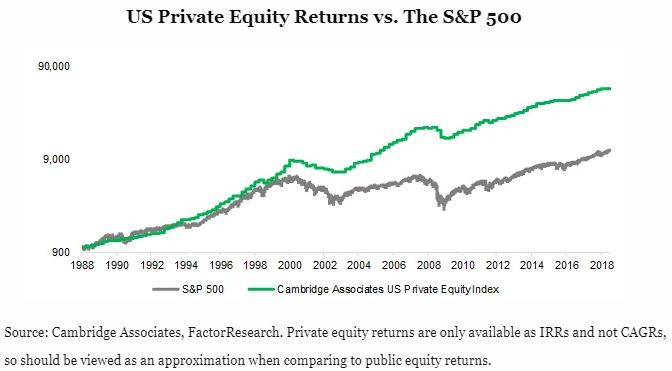

As evident in Figure 2, the PE sector has been outperforming the broad equity market for most of the years in the past and it is my prediction that it will continue to do so for many years to come. There are two main reasons for this which are a) low-interest rates environment and high equity prices place a cap on the expected returns of the conventional asset classes such as public equities and fixed income and b) increasing rate of success (or exits) by companies backed by VCs. In other words, the value created by VC backed technology companies is increasingly being realised and being returned to the early founders and investors. (see Figure 3 below).

We are also seeing an increase in IPOs being chosen as an exit route (Figure 4), opening an opportunity for the public to access the potential future upside but often times this is after the top of the cream has been taken off by the big winners (the founders and their early investors). In other words, it is still unknown whether the companies that went public will continue to produce exceptional value in a similar magnitude compared to value realised via the IPO. This means that the best and the biggest opportunity still lies in by investing in companies while they are in the private market, an area that is accessible to only a small percentage of our population.

How?

Increase fund allocation to PE

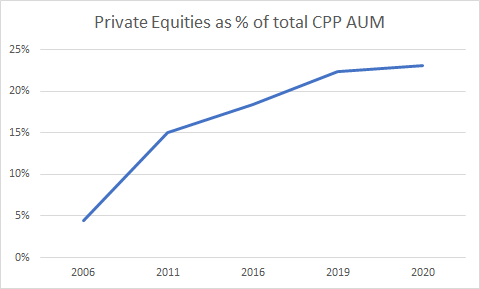

The most obvious way for pension funds to protect its interest (in case of CPP, its 20m participants) is therefore by increasing its fund allocation to PE. As can be seen from Figure 4, CPP has fortunately been increasing its asset allocation to the PE sector.

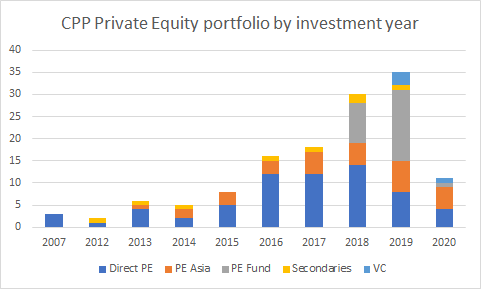

As can also be seen from Figure 5, we are also seeing the CPP’s PE sector’s investment activity is increasing. It is particularly encouraging to see that CPP has recently introduced a VC specific team with their office in San Francisco. The PE sector is also making some exciting and promising investments such as its recent US$2.25b investment in Waymo, Google’s self-driving project. Without involvement through CPP, the Canadian public would not have been able to have access to such promising investments.

Increase global footprint

This is another area which large pension funds such as CPP should focus on to capture future opportunities in the private market. This is inevitable as the value is being created from all over the world. CPP has done well in this regard too as they now have 9 office around the world and investments made in 55 different countries directly or along with its 283 global investment partners. Such diversification and global footprint are well represented by the change in CPP’s geographical asset allocation over the past decade or so. See Figure 6.

Hire people with technology/entrepreneur background

One area I think the pension funds, including the CPP, could improve on is to hire more people with technology and entrepreneurship background. Pension funds historically hired mostly talents from banking and consulting background which is understandable because its investment exposure was largely towards conventional assets such as fixed income and public equity. However, as argued above, the importance of PE, especially those of early stage in the technology industry increases, the need for talents who have built, failed and/or exited a company from scratch will be of increasing value to the fund.

Remaining questions

While I have written above some of my observations and conviction, by no means it is the correct answer nor is it the end. Below are some of the continued questions that I think practitioners in the pension fund industry, especially those in the PE sector, should be asking:

- Where would future returns (alpha) likely generate from?

- How and why has PE been viewed as a riskier investment? (i.e. high risk/high return is bull shit) Could or should it change in the future?

- To what extent would the traditional portfolio theories and data based on history be applicable in future, especially in the PE sector?